I had the privilege this week of being asked to speak at the conference Treating Vulnerable Customers Fairly, where I shared a session with the brilliant Bailey Kursar of Touco, who works on inclusive design, the subject of our panel. I want to share my talk in full, because this is such an important subject. It is also one that Rogue Interrobang is very happy to speak to your teams, or consult with your organisation about – especially those of you in the financial services sector, because enabling everyone to access services like these benefits everyone.

It’s a real pleasure to be here. I’m an expert by experience – I’m bipolar, ADHD and dyspraxic. In that capacity, I am a member of the Advisory Board of the Money and Mental Health Policy Institute, contributed to the Oxford Disability Law Project’s policy paper on the impact of Covid on disabled people, and have been working with groups like the Money advice Trust on the relation between disability and financial inclusion for over 15 years. But I’m also a specialist in the relations between creativity, communication, and inclusion, in which capacity I’m the CEO of only the second spinout company from Oxford University’s Humanities Division.

I want to take a very simple approach to what it means to be a disabled customer, with a particular focus on mental illness and neurodivergence. I have just two main slides that go together very straightforwardly. The first takes four ways the experience of dealing with financial services disables us. I will give very brief examples, from my own experience and that of other disabled customers. And then I’ll look at the ways in which better design of that interface between us and financial services could, rather than disabling us, enable us.

What I want to say is based around the social model of disability. That is, rather than seeing us as “having a disability” which makes it hard for us to access certain goods and services I will look at the way we are disabled by goods and services that are not set up so that we could access them in the same ways others can.

In some ways this can make for uncomfortable listening, because it places responsibility with people who design things. But for the same reason it can be a positive account because it shows the ways in which those designers can make a real difference in enabling us.

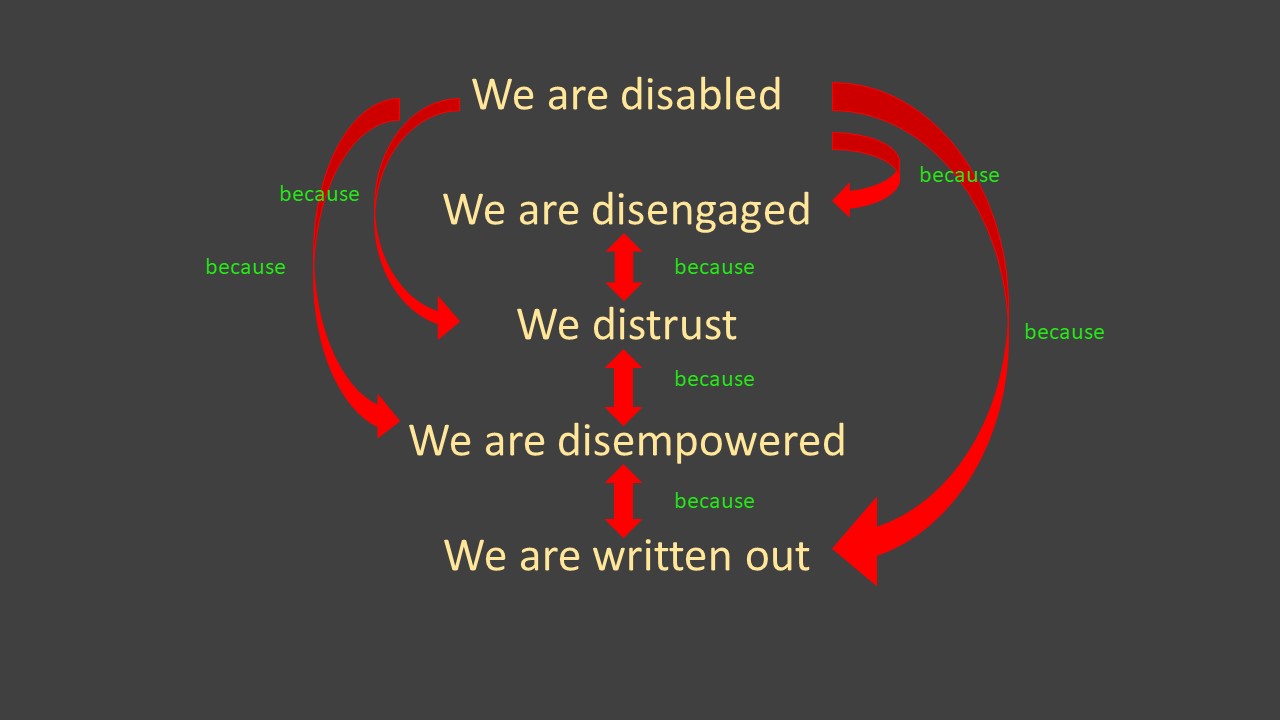

So here is the first slide. I have highlighted four things that disable us, and the arrows I’ve drawn between them show how interconnected they are. Which means they are liable to feedback loops, which can be vicious or virtuous.

First, we are disabled because we are disengaged. Disengagement is one of the biggest challenges financial service companies face when dealing with disabled customers. For many of us, disengagement is a result of simply not being able to engage because our communication needs are not catered for. Or, even if a company would provide accommodations if asked, that means that before doing something as simple as basic communication, we have to make a whole series of calculated choices about disclosure and the possible consequences, knowing that the moment we disclose, we cannot take it back. That makes engaging utterly exhausting in a way for most people it just isn’t.

Which leads to distrust. When you have a mental illness, or when you’re dyslexic, autistic, or ADHD, it goes with the territory that you experience prejudice and judgement – sometimes on a daily basis. This is often down to what I call the empathy gap – the fact that the easier most people find it to do something, the harder it is for them to imagine what it would be like not to be able to do that. So when they encounter us, saying things they don’t understand – like “I can’t use the phone” or “just because I can’t find my paperwork that doesn’t mean I lack mental capacity” they make assumptions, and often those assumptions can lead to disastrous first contacts, and once we’ve been through that once it will take a lot for us to trust talking openly again.

We are disempowered when we don’t have control of our data. We see this in many circumstances. First there are those situations when we are made to repeat deeply distressing and personal details simply to access a basic service because we have not been given an opportunity to “tell it once” – or, if there is such an opportunity, it is not sophisticated enough to distinguish between “I want you to remember that I need to communicate by webchat” but “I do not want you to give me less favourable pricing because you know I am mentally ill”.

And second, we see it in the exploration of “helpful” anticipatory measures that seek to predict and avoid problems we might face by using machine learning to analyse our behaviour and figure out any problems we have. This, like the rise of the wellness app, is part of techbro culture that sees us – if at all – as a fascinating object of engineering and not as subjects – of our own lives and our own data. If disabled people are not embedded in the very fabric of these projects at every level to the most senior they will not serve our needs. We understand you may still wish to do them for your own bottom line, but when you then trumpet them as for our benefit – well, see above about distrust and below about writing us out.

We are written out when communication simply doesn’t acknowledge our needs exist. The result is to send a very clear message that we haven’t even been considered. Imagine a “contact us” page on a bank’s website (something I encountered just last week) that only has telephone numbers. If it’s that clear a bank doesn’t think about our communication needs, it shows where their priorities lie – and sends the message they probably aren’t considering us in other areas as well. In which case when they give their glossy slogans about valuing their customers, the implied message is very clear – “we don’t mean you”.

One of the clearest ways we have been written out widely in recent years is the growth of the wellbeing movement – and associated apps. Wellbeing is great, but in so many places – and, sadly, budgets, wellbeing and “mental health” have taken the place of provision for those who are mentally ill. Money – and attention – have gone into keeping the essentially “well” well at the expense of the sick and disabled. And often claims about universal design have compounded the issue, ignoring the very specific and often very different needs of disabled people.

And the sum of these is that we experience very specific disadvantageous outcomes such as penalty charges, having to give extra information to access the same service by repeating ourselves, not using some banks or services at all

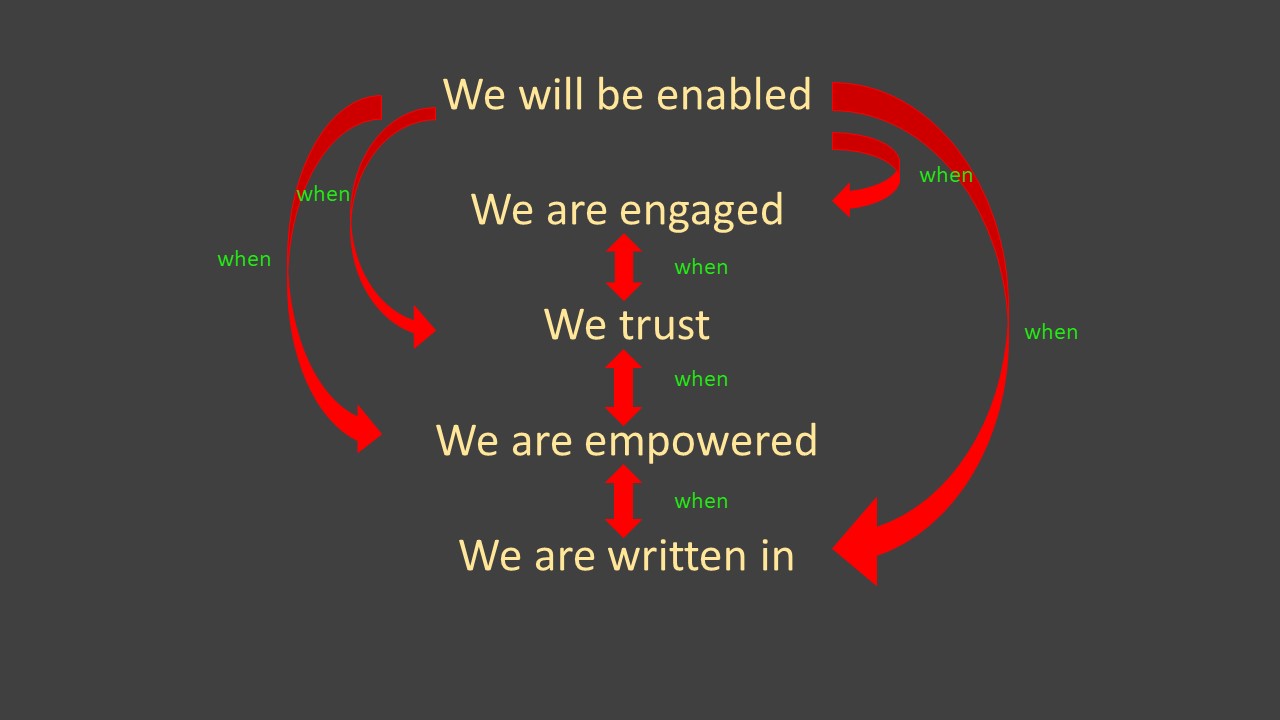

The flip side of this, though, is that it is possible – through the way you design your products, services, and the delivery of them – to enable rather than disable us.

You can engage us when you offer us the communication channels we need. And when you do as much pf that as you can as defaults. If you make people ask for what they need, then you are bringing every question about disclosure in people’s heads into play.

We will trust you when we receive no judgement or hint of judgement. And most important, trust is built when words and deeds match. This is especially true with many neurodivergent customers. Greta Thunberg speaks a lot about the way politicians say one thing and then act in a way that suggests their words are meaningless. Often neurotypical people don’t even realise they are doing it, but we do. When you say “we really welcome autistic customers” but then fill your contact page with only telephone numbers your autistic customers will see the lie in your words that you don’t even realise is there. And that, of course, is why you need not just to treat this talk as a checklist – what you actually need is to engage autistic, ADHD, dyslexic, mentally ill people to co-design things with you.

We will be empowered when you let us decide how our data should be used. This means not just telling us how you will use data, including and especially the sensitive personal data about our disability and asking us to consent, but giving us a range of options and asking us which we would like. It can be a simple set of options – to help you offer more appropriate products, to help with interactions, to enable us to receive fast tracked support if we need it but not before, and so on. That kind of empowerment will lead to greater engagement because we won’t be worrying every time we get in touch that we will have to repeat distressing parts of our history that we have already been through. Dealing with our bank will be reduced – and I mean that in the very best way – to just dealing with our bank.

And we will be written in when we receive communications from you, or go to your website, and instead of the overwhelming sense of absence we get too many times at the moment from exploring and exploring and still finding nothing for us, we will find the small cues (“give us a call or chat to us using our webchat”) that mean we are part of the existing and potential customer base you have thought about.

To help with writing us in, at the start of the pandemic, I created a communications toolkit for organisations to help them avoid unintentionally excluding or alienating disabled people in their audiences. You can download it from the QR code on this slide.

The final point I want to make is the most important. Many of these steps, while simple, are nonetheless hard. And they can be a hard sell to senior teams. Especially if neither you nor they can “feel” the need for them, from the inside. And the answer to that, and to making decisions that really work for disabled people, and enable us to become not just problems you can cope with but flourishing customers who contribute to your business, is to ensure that we are always involved – not just consulted but in the room and making the decisions, at whatever level they are made.

Leave a comment